We all want our money to work as hard as we do. It's a great feeling to know that while you're sleeping or spending time with family, your savings are building momentum in the background. Understanding the mechanics of this growth is the first step toward true financial wellness and creating a life that reflects your values.

What is compound interest?

Compound interest happens when your initial savings and any interest it accumulates grows even more interest. This means that each time you earn interest, it automatically gets added to your account balance and becomes part of the principal for the next calculation.

Think of your savings as a snowball rolling down a hill. The farther it travels, the more snow it accumulates, and the bigger it grows. That's exactly how compound interest works for your money.

How the math works

If we boil down the concept to its absolute core, compound interest is "interest on interest." While the concept is simple, the math behind it involves a specific formula. For the do-it-yourselfers who love to see the mechanics, here's the formula:

A = P (1 + r/n)^(nt)

- A = Final amount

- P = Principal sum (the amount you start with)

- r = Annual interest rate (how much the bank pays you)

- n = Number of times interest is applied per compounding period

- t = Number of compounding periods

If you prefer to skip the lengthy formula, Investor.gov has a free calculator you can use to run your own numbers quickly.

A real-world example of compounding

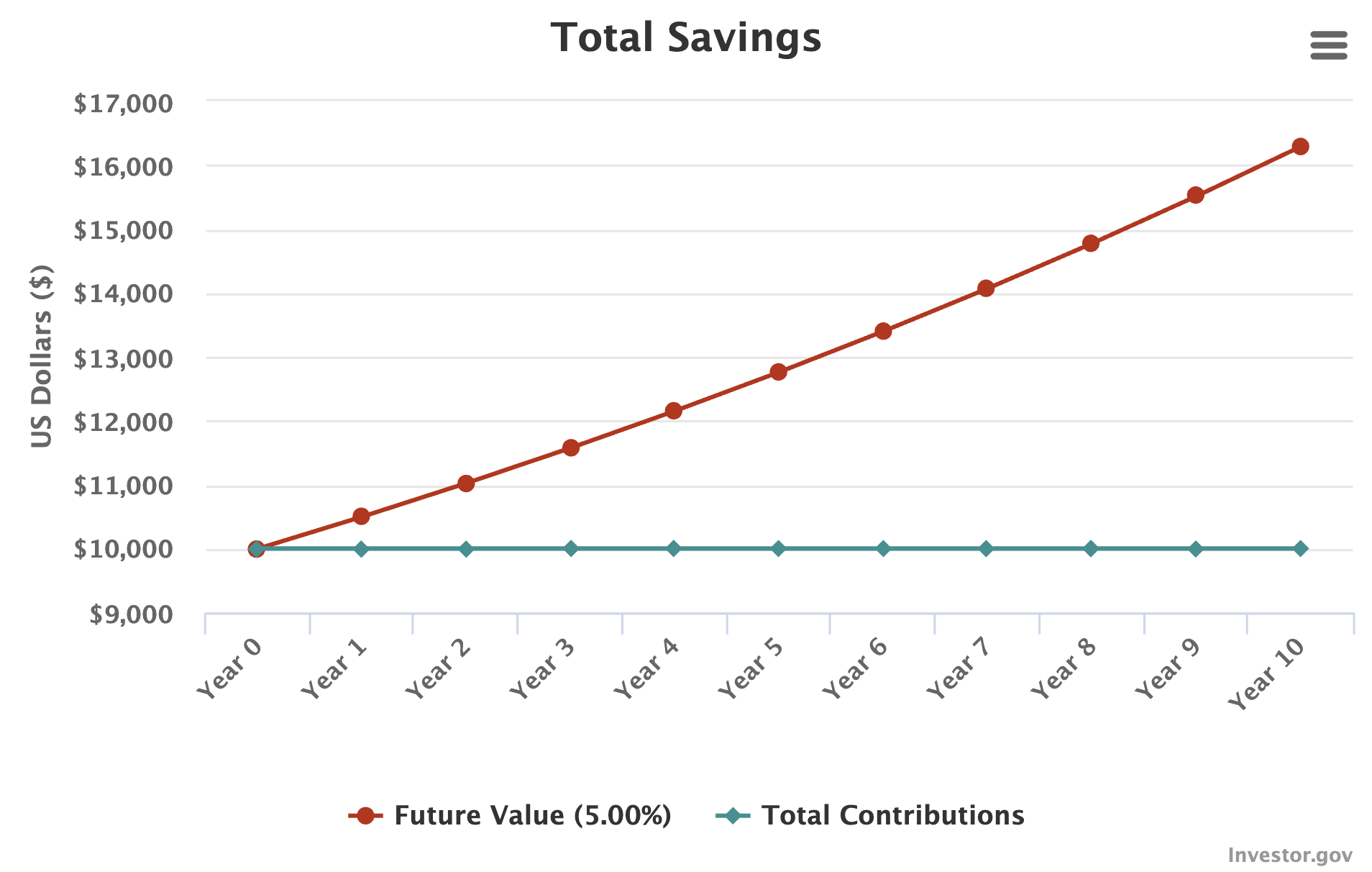

Let's look at a specific scenario to see the power of compounding in action. Imagine you open an account with $10,000 at an annual interest rate of 5%, compounded monthly. You hold this investment for ten years. At the end of those ten years, you'll have $16,470.09.

Here's how that growth happens. In the first year, you made $511.62. As time went on, your interest continued to generate more interest, accelerating the growth of your balance without you adding another penny.

| Years | Future Value (5.00%) | Total Contributions |

|---|---|---|

| Year 0 | $10,000.00 | $10,000.00 |

| Year 1 | $10,511.62 | $10,000.00 |

| Year 2 | $11,049.41 | $10,000.00 |

| Year 3 | $11,614.72 | $10,000.00 |

| Year 4 | $12,208.95 | $10,000.00 |

| Year 5 | $12,833.59 | $10,000.00 |

| Year 6 | $13,490.18 | $10,000.00 |

| Year 7 | $14,180.36 | $10,000.00 |

| Year 8 | $14,905.85 | $10,000.00 |

| Year 9 | $15,668.47 | $10,000.00 |

| Year 10 | $16,470.09 | $10,000.00 |

Source: Investor.gov

(Note: This is a hypothetical mathematical example for illustrative purposes only and does not represent the return of any specific investment.)

Compound interest vs. simple interest

If you're wondering how this differs from simple interest, here's the breakdown. Simple interest generates new interest each year based only on your original principal. It doesn't get added back to the balance to earn more money.

Using the same scenario above ($10,000 at 5% for 10 years), if your account received simple interest, $500 would be added to your account every year. Your final value would be $15,000.

Because of the monthly compounding in the first example, you'd have made $1,470.09 more than you'd have with simple interest, ending with that total of $16,470.09.

The Rule of 72

The Rule of 72 is a quick calculation to estimate how long it would take for your money to double. Simply divide 72 by your interest rate to see the timeline for growing your savings twofold.

For example, if you have $1,000 with a 5% interest rate, it would take 14.4 years to turn into $2,000. (Note: This is a hypothetical mathematical example for illustrative purposes only and does not represent the return of any specific investment.)

(Calculation: 72 / 5 = 14.4 years)

Timing matters: When is interest credited?

Compounding periods designate how often interest is added to an account. The intervals vary widely. Interest can be compounded annually, semiannually, quarterly, monthly, daily, or even continuously.

It can get complex, however. For example, interest might grow daily but only be added monthly to the account. This is important because your interest can't earn more money until it's officially credited to your account.

Here's how frequently interest is added to common financial instruments:

- Certificate of deposit (CD): Standard CD compounding frequency schedules are usually monthly or daily.

- Series I bonds: Interest is compounded every six months (semiannually).

- Savings and money market accounts: The frequently used compounding period for bank accounts is daily.

Common accounts that earn compound interest

There are several conventional ways to start taking advantage of this growth:

- Traditional savings accounts: These offer the lowest interest rates but typically carry zero risk and are FDIC insured if purchased through most banks.

- Certificates of deposit (CDs): They're also generally safe and FDIC insured but may require you to lock up your money for a set time.

- Money markets: They're similar to savings accounts but often offer better yields that vary by institution.

- High-yield savings accounts: These typically offer more competitive interest rates than traditional savings, CDs, and money markets. Since the compounding period is often shorter, you may be able to grow your money faster.

- Bonds: Fixed-income investments can also generate compound interest. To receive compounded interest with bonds, you'll need to reinvest your interest payments. Bond funds (mutual funds) can be a good substitute for individual bonds here.

The Facet difference

At Facet, we believe your financial roadmap is about more than just math or interest rates. It's about your life. While banks focus on numbers, you'll work with a CFP® professional to ensure every part of your financial life serves your personal values.

Our membership model charges a flat fee, which means we don't sell products or earn commissions on the investments we recommend. This allows us to offer advice as a fiduciary, meaning every recommendation is made truly in your best interest. Whether you want to learn more about Facet's short-term investment strategy (keeping in mind that all investing involves risk, including the possible loss of principal), maximize your savings, or navigate a major life transition, we're here to help guide your journey with confidence.