We all know that bringing a new life into the world is a big financial commitment, but it's also one of the most rewarding journeys you'll ever take. It's completely normal to look at the price tag of raising a family and feel a mix of excitement and anxiety. We want to validate that feeling and help you move past the sticker shock so you can focus on building a roadmap that aligns with your values and dreams.

What the numbers say about raising a family

We all know that raising kids is expensive, but it helps to look at the specific data. In 2015, the US Department of Agriculture estimated that the typical middle-income family would spend an average of $233,610 to raise a child to age 17.

However, we have to look at the current reality. When we factor in the inflation rate, parents of a child born in 2022 could expect to spend an average much closer to $300,000. It's important to note that this estimated cost doesn't include college costs.

With that said, chances are that averages won't apply to your unique situation. You could very well spend more or less depending on your choices. One of the biggest factors that impact this average is simply the kind of life you want to give your child.

Defining the life you want for your children

Many prospective parents envision the life they want their child to have based on their own upbringing. It's a deeply personal reflection.

Do you envision a childhood filled with private schools, horseback riding, and tennis camps? Or do you see a home where parents provide the necessities and children work for luxuries, or perhaps something in-between?

Long before the baby arrives, it's helpful to have in-depth discussions with your partner about:

- How each of you were raised

- How you want to raise your children

- Your hopes and dreams for them

- The number of children you want

- The experiences you want them to have

Planning for the cost of having children doesn't stop when you finish decorating the room or buying diapers. It continues throughout every milestone of your children's lives and requires careful planning. Every decision you make will have a ripple effect on the amount you spend.

How your decisions drive your budget

In some ways, asking about the cost of raising a child is similar to asking how much money you need to retire. Is your retirement going to consist of long, lazy days fishing in a local river, or do you plan on traveling the world with your partner and enjoying fine restaurants? Those two alternatives require very different budgets.

Similarly, the cost to raise a child varies widely based on the trade-offs you make. For example:

- Will you need a bigger place to live or want to move to an area with better schools?

- Do either of you have strong feelings about public school vs. private school?

- Will you pay for childcare expenses or will nearby family members lend a hand?

- Will you need to buy a family-friendly car?

The best time to make those decisions is before your child is born. Before the baby arrives, start getting a handle on what their arrival will mean financially. This is the time to set up your initial financial roadmap, including expenses you might not have thought of like health insurance and estate planning.

Understanding childcare and education costs

When it comes to setting up a planning strategy, it's important to pay particular attention to childcare unless one parent is going to be a stay-at-home caregiver. Household income will likely play a major factor in whether you can fulfill your ideal scenario.

Childcare expenses

Sources: LendingTree analysis of U.S. Census Bureau, Massachusetts Institute of Technology (MIT) Living Wage Calculator, Care.com, U.S. Bureau of Economic Analysis, Kaiser Family Foundation and Tax Foundation data.

According to the World Population Review, the average cost of providing center-based childcare for an infant in the US is $1,230 per month. While your costs may vary widely from the average on a state-by-state basis, childcare can cost between $5,436 and $20,913 per year.

Education expenses

Next up in your timeline comes your child's education. Private elementary school (kindergarten to sixth grade) tuition costs can range from just under $10,000 per year in relatively lower-cost areas to more than $30,000 per year in cities like New York or San Francisco.

This amounts to an easy six-figure spend for seven years of education. When you consider private middle and high school, this can double the cost. In fact, top-tier private schools can cost just as much as some four-year colleges.

Buying a home in a place where public schools are better may cost more, but the savings in not sending your child to a private school may offset that. Alternatively, choosing cheaper vacations in the US instead of traveling to other countries may help save money to put toward college tuition.

Where the money usually goes

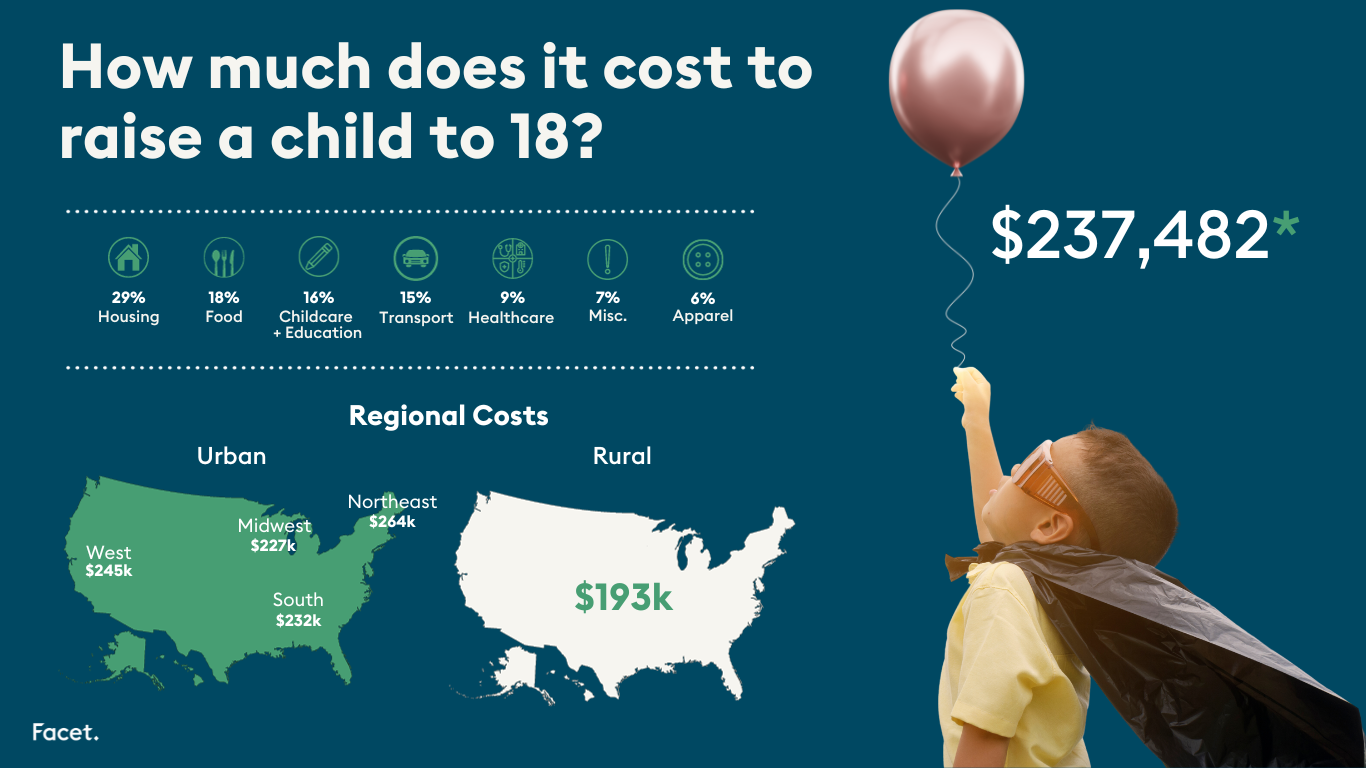

The US Bureau of Labor Statistics publishes a wealth of data in its Consumer Expenditures Survey that helps break down where money flows. Although many families will spend more or less than the average, surveys show that housing costs are the biggest expenses in raising a child for middle-income families, representing 29% of all child-related spending.

Food comes in second at 18%, and childcare and education is third at 16%.

The teenager factor

One surprising data point is that teenagers tend to cost about three times what babies do per month because they have additional expenses. If you add a teenage driver to your auto insurance policy, you'll understand why.

Economies of scale

There is some good news for parents planning a larger family. When it comes to children, there are economies of scale when you have more than one. Families tend to spend less on the second child than they did for the first.

Federal surveys show that for two-parent families with one child, expenses averaged 27% more per child than expenses in a two-child family. For families with three or more children, expenses averaged 24% less per child than for a child in a two-child family.

Each additional child costs less because children can share a bedroom, families can buy food in larger quantities, and clothing and toys can be handed down. Children may not be cheaper by the dozen, but the cost per child definitely drops.

The Facet difference

At Facet, we believe that understanding the cost of raising a family shouldn't be a source of fear. It should be a tool for empowerment. Traditional financial advice often overlooks the day-to-day cash flow realities of raising kids, focusing only on investment management. We do things differently.

Our membership model pairs you with a CFP® professional who looks at your whole life—from budgeting for childcare to saving for college—without charging you a percentage of your assets. We're here to help you build a roadmap that balances your financial health with the life you want to live today.