Receiving equity compensation feels like a huge win, but it can also feel overwhelming when you stare at the fine print. It's completely normal to feel a mix of excitement about the potential wealth and confusion about the tax rules or vesting schedules. You aren't alone in trying to decode this part of your financial roadmap, and understanding the details is the first step toward making your money work for your values.

What are restricted stock units (RSUs)?

Restricted Stock Units (RSUs) are a popular way for companies to attract and retain talent by offering ownership incentives. Think of them as a promise: the company sets aside shares for you, but you don't actually own them until you fulfill certain milestones or stay employed for a specific timeframe.

The basics of RSUs

Here is the most important thing to know: RSUs represent shares of stock, but they have no intrinsic value to you until they vest. Vesting simply means you have met the time or performance requirements to take full ownership.

Once vesting takes place, those shares are considered income. Because of this, companies typically withhold a portion of the shares to cover income taxes. You then receive the remaining shares and have the right to do whatever you wish with them. You can sell them immediately, hold them for potential growth, or use them to fund other goals on your financial journey.

Why companies offer RSUs

Companies use RSUs to encourage you to stay for the long haul. This type of compensation gained significant popularity in the mid-2000s following accounting scandals involving companies like Enron and WorldCom.

From the company's perspective, RSUs offer several benefits:

- They reduce the immediate administrative burden.

- They provide an incentive for you to help the company perform well since the value of your shares can increase.

- They defer the issuance of shares until a later date, which helps delay stock dilution for existing shareholders.

How vesting schedules work

Vesting schedules are the timeline for when you can actually access your RSUs. There are two main types you'll likely encounter: 'graded' and 'cliff' vesting.

Graded vesting

In a graded vesting schedule, you receive a specific percentage of your shares periodically, usually on the anniversary of the grant date. A typical duration ranges from three to four years. For example, on a 3-year graded schedule, 33.3% of your RSUs might vest every year.

This incremental approach is great because it gives you access to a portion of your RSUs over time. This helps smooth out the impact of stock market fluctuations and gives you a more predictable stream of income.

Cliff vesting

Cliff vesting is an all-or-nothing approach. You receive your entire allotment of RSUs only after a set period or once a specific milestone is achieved. If you leave the company before that date, you typically forfeit everything.

This can be challenging because it requires a longer commitment before you see a dime of value. However, the financial reward can be significant if you stay for the required period.

A real-world example

A common setup involves a one-year cliff followed by a four-year schedule. Here is exactly how that looks for an employee granted 2,000 shares:

| Grant Date | Shares Granted | Vesting Dates | Shares Vesting | Unvested Shares |

|---|---|---|---|---|

| 6/1/2021 | 2,000 | 8/1/2022 | 500 | 1500 |

| 8/1/2023 | 500 | 1000 | ||

| 8/1/2024 | 500 | 500 | ||

| 8/1/2025 | 500 | 0 |

In this scenario, the employee didn't get anything until over a year later on 8/1/2022. After that initial cliff, they received 500 shares annually until all 2,000 were vested. If this employee were to leave before the four years were up, they would forfeit any unvested shares.

The tax rules you need to know

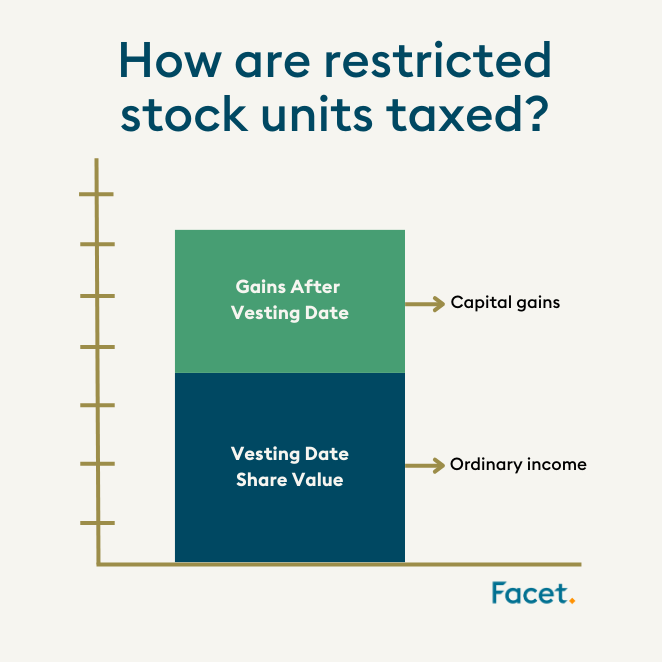

Taxes are due at two distinct moments: when the shares vest and when you sell them. Managing this correctly is critical to your financial wellness.

Taxes at vesting

The value of your vested RSUs is treated as ordinary income. Here is the formula to figure out what is taxable:

- Determine the fair market value (FMV) of the RSUs on the vesting date.

- Subtract any amount you paid for them (usually zero).

- Apply your applicable tax rate.

The standard approach is for the employee to relinquish a portion of the stock back to the company to cover the bill. The company then uses that cash to pay federal income tax, state and local taxes, and Social Security and Medicare taxes.

Capital gains and losses

When you decide to sell your shares, you enter the world of capital gains. You will be taxed on the difference between the sale price and the fair market value on the day they vested.

The applicable tax rate for capital gains can be as low as 0% or up to 20%, depending on your income. It's smart to consider tax-loss harvesting here. This strategy uses capital losses to offset potential gains. By realizing losses, you can:

- Reduce your overall taxable income.

- Potentially lower your tax bill.

- Use capital losses to offset up to $3,000 of regular income for tax purposes.

Facet is not an attorney and does not provide tax or legal advice. Consult a qualified tax or legal professional regarding your specific situation.

RSUs vs. stock options

RSUs are often compared to Non-Qualified Stock Options (NSOs) and Incentive Stock Options (ISOs). While both are equity compensation, they work differently.

Advantages of RSUs

The biggest plus is that RSUs usually don't require an upfront purchase. You don't have to buy the stock; it's given to you. This means RSUs retain value as long as the stock price is above zero, offering a level of security that options don't always provide. They are also generally more straightforward to understand.

Drawbacks of RSUs

There are some downsides to consider:

- They may incur a higher tax burden than stock options.

- You face uncertainty regarding the share value before you can sell.

- Sudden valuation declines can wipe out value.

Strategies for managing your shares

To make the most of your RSUs, you need a roadmap that goes beyond just hoping the stock price goes up.

Diversification is key

We generally recommend that you don't rely solely on your company's stock. Diversifying your investment portfolio helps you:

- Mitigate losses in a declining market.

- Control the exposure of your RSUs in your portfolio.

- Capitalize on potential growth in other sectors.

A smart move is to sell RSU shares when they vest and invest those proceeds into a diversified portfolio. This reduces the risk of having too much of your financial future tied to a single company's performance.

Special circumstances

Life happens, and it's important to know how events like death, disability, or job transitions affect your equity.

Death and disability

If you pass away, RSUs typically vest and become payable to your estate or beneficiaries. In the case of disability, the rules depend entirely on your specific stock plan and grant agreement. Be sure to review your documents so you know what to expect.

Job changes

If you switch jobs, you usually forfeit any unvested shares. However, in some cases, a new company may offer to buy out your unvested RSUs as part of a compensation package to get you to switch. It is crucial to check your specific terms before making a move.

The Facet difference

At Facet, we believe your equity compensation is just one part of your larger financial life. Traditional advisors might just tell you to sell or hold, but we look at how those decisions impact your taxes, your retirement, and your personal goals. Our flat-fee membership model means we don't charge a percentage of your assets, aligning our guidance with your best interests and focusing on helping you build the life you want.