It is incredibly exciting to land a promotion, change jobs, or reach a new career milestone that comes with a higher salary. You have worked hard for that progress, and it feels completely natural to want your daily life to reflect that success. If you have noticed that your bank account doesn't seem to be growing despite your higher income, you aren't alone, and it doesn't mean you are bad with money.

What lifestyle creep actually looks like

As you progress in your career and hit major life milestones - like marriage, starting a family, buying a new home, or saving for college - you naturally have more options for how to use your money. The trap, however, is what we call "lifestyle creep."

Simply put, lifestyle creep is when your expenses inflate to fill the space created by your extra income. It is the classic case of "make more money, spend more money." But it's not just about spending; it's about spending without a roadmap.

The biggest mistake people make when they earn more is that they spend the new money first and then look to save whatever is left. Often, those new expenses creep up higher than expected, leaving nothing left to save for the future. One day, you might realize you are making more than ever, but you don't have much to show for it.

Spending more money isn't necessarily a bad thing. It only becomes a problem when you overspend to the point where you can't save for what you really want, like your retirement or a rainy day fund. The decisions you make today have a ripple effect that can impact you for years to come.

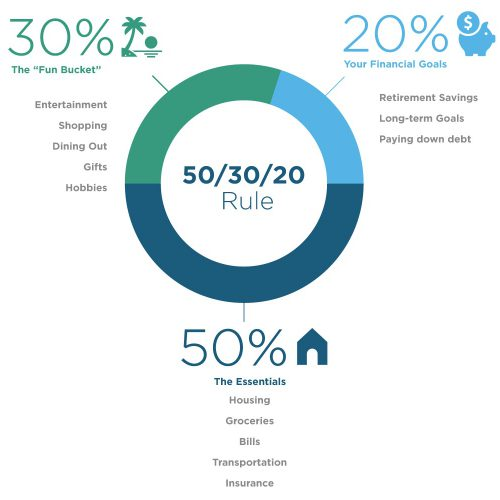

Where things go wrong: The 50% and 30% rule

To understand how this happens, we need to look at where the money actually goes. There are typically two main areas where lifestyle creep takes hold.

1. The big 3 expenses

There are three categories that make up almost 50% of your ideal spending plan: housing, transportation, and food. Because these buckets are so large, lifestyle creep here can hit your finances quickly. As your income increases, it's tempting to look at a bigger home, a nicer car, or frequent dining out. While these upgrades might look affordable on paper, you need to plan carefully to ensure they don't permanently inflate your lifestyle beyond what is sustainable.

2. The other stuff

The smaller expenses generally make up 30% of your ideal plan. These are the ones that sneak up on you, not individually, but collectively. If you have ever muttered the phrase "it's just..." before buying something, you might be experiencing lifestyle creep.

You might say, "It's just" $100, what's the big deal? Or you might convince yourself that a nicer car is "just another $200" more per month. It is very easy to go from "it's just" to "it's now" a problem.

6 questions to ask yourself to avoid the trap

If you think lifestyle creep won't happen to you, it's worth taking a moment to reflect. Ask yourself these six questions to see if you are at risk.

1. Are you spending emotionally?

Have you ever made an emotional purchase or regretted buying something? Buyer's remorse is a strong sign that lifestyle creep might be popping up, especially if it happens more than once.

It is also helpful to ask: Have you ever wondered why you think, feel, or act the way you do when it comes to money? This is the psychology of money, and it drives your decisions. Knowing what makes you tick financially can make a world of difference in avoiding unhealthy habits.

2. Are you prioritizing value over "things"?

Have you bought something you always wanted, only to find it didn't really make you happier? Nicer things are okay, but they often aren't the source of true happiness. Increased fulfillment comes when you align your money with what you value and the life you actually want for your family.

3. Are you trying to keep up with the Joneses?

Have you looked at something a neighbor or friend owned and thought, "I should get one of those, I can afford it"? Keeping up with the Joneses is a real phenomenon. If you make decisions just to keep pace with those around you, you may end up building a lifestyle you can't actually sustain.

4. Are you sticking to your roadmap?

Have you ever struggled to pay for something you really wanted because you spent too much on something you didn't need? Overspending can deprive you of the things that are truly important, like a nice vacation, your next home, or contributing to your children's college fund.

5. Do you understand your debt?

Have you ever found yourself spreading payments out on a large purchase because you didn't have the cash on hand? Not all debt is bad debt, but loan payments can add up faster than you think. It is crucial to keep an eye on your total recurring monthly expenses.

6. Do you have a holistic plan?

Have you made a purchase and then realized there were other expenses you didn't account for? For example, a bigger house means more furniture, higher utility bills, more maintenance, higher insurance premiums, and more taxes. These "extras" can add up quickly and need to be part of your roadmap before you sign any loan papers.

Without a plan, it is hard to see how new expenses affect the rest of your financial landscape. As expenses add up, they can eat into your ability to save for key life milestones.

Why a dedicated guide makes a difference

At Facet, we believe that avoiding lifestyle creep isn't about restriction; it's about empowerment. It is about understanding how every financial decision affects your entire life, both now and in the future. That is why we don't just hand you a static document and walk away.

Our membership model pairs you with a dedicated CFP® professional who works with you to build a dynamic roadmap. We operate on a flat-fee basis, which means our advice is objective and focused on your best interest. We help you weigh your options - like that new car or home upgrade - so you can make smarter decisions that put you in control of the life you want.