The decisions we make with our money are deeply affected by the prices we pay for everything, from our morning coffee to the homes we live in. Over time, prices tend to creep up so gradually that we often don't notice the changes week to week, but understanding this mechanic is the first step to feeling confident about your financial future.

What exactly is inflation?

Let's skip the economic jargon and keep it simple: inflation is when things cost more than they used to. That fact alone isn't inherently good or bad, but it has a very real impact on your wallet. It means that every dollar you have today will likely buy a little less tomorrow. You might hear financial pros refer to this as a reduction in your purchasing power. Regardless of how you look at it, what you do with your money - whether you spend it, save it, or invest it - has real implications for your future comfort.

What causes prices to rise?

There are many factors at play in our economy, but you really only need to understand two basic concepts: "cost-push" and "demand-pull." Here is how they break down.

Cost-push inflation

This occurs when it costs a company more to provide a good or service. Maybe the cost of raw materials went up, so they raise their prices to compensate. Higher costs literally push the price of the things we buy higher.

Think about your iPhone for a second and all the parts required to make it. Now, assume that the cost of the battery or the computer chip inside it increases in price. Eventually, Apple will pass those higher prices on to us.

Demand-pull inflation

This happens when our desire to buy things - our demand - is greater than what companies can provide, which is their supply. Because something is in short supply, people are willing to pay more to get it. In this situation, we pull the price higher.

Let's look at car prices as a recent hypothetical example. New cars increased in price by over 6% from July of last year to July of this year due to chip shortages and more expensive tech packages. As a result, more car buyers looked at used cars to save money. However, due to the pandemic, used car inventory - supply - was down as rental car companies held onto their cars and didn't sell them into the used car market. Higher demand and lower supply led to a 41% increase in used car prices over that same period.

Can anyone control inflation?

The short answer is kind of. Controlling or influencing inflation is more of an art than a science. This is one of the reasons why we have the Federal Reserve (the Fed), our central bank. The Fed's job is to promote healthy levels of employment and inflation, which they call price stability. The primary tool at the Fed's disposal to influence inflation is interest rates, which is why you'll often hear the two mentioned together in the news.

As the economy grows and "heats up" and people spend more, we typically see an uptick in inflation. As inflation rises, the Fed can raise interest rates to help constrain or "cool off" the economy, resulting in lower inflation. Conversely, if the economy slows down, the Fed can lower or "cut" interest rates to help stimulate the economy. It's a little like Goldilocks. The Fed keeps trying different policy measures and then tests the economy to see if it's too hot, too cold, or just right.

Is inflation actually a good thing?

Believe it or not, a small amount of inflation - around 2% - is generally believed to be "just right" or good for the economy. Why is this the case? First, it's better than deflation, or falling prices. If companies have to lower prices, they make less money and eventually have to lay off workers. Second, rising prices create an incentive to buy more things today. This leads to higher demand, which boosts consumer spending, and all of this drives economic growth.

You might be asking, "But doesn't inflation mean my money is worth less?" The short answer is yes. The longer answer is that a healthy level of inflation is generally offset by higher wages and interest rates. This means your cash and bonds pay more, so it all evens out in the short term in most cases. Over the long term, however, inflation is a very powerful force as it reduces how much each dollar is worth. This is why having an appropriate investment strategy to grow your money by more than the rate of inflation is an essential piece of your overall financial roadmap.

How we measure the cost of living

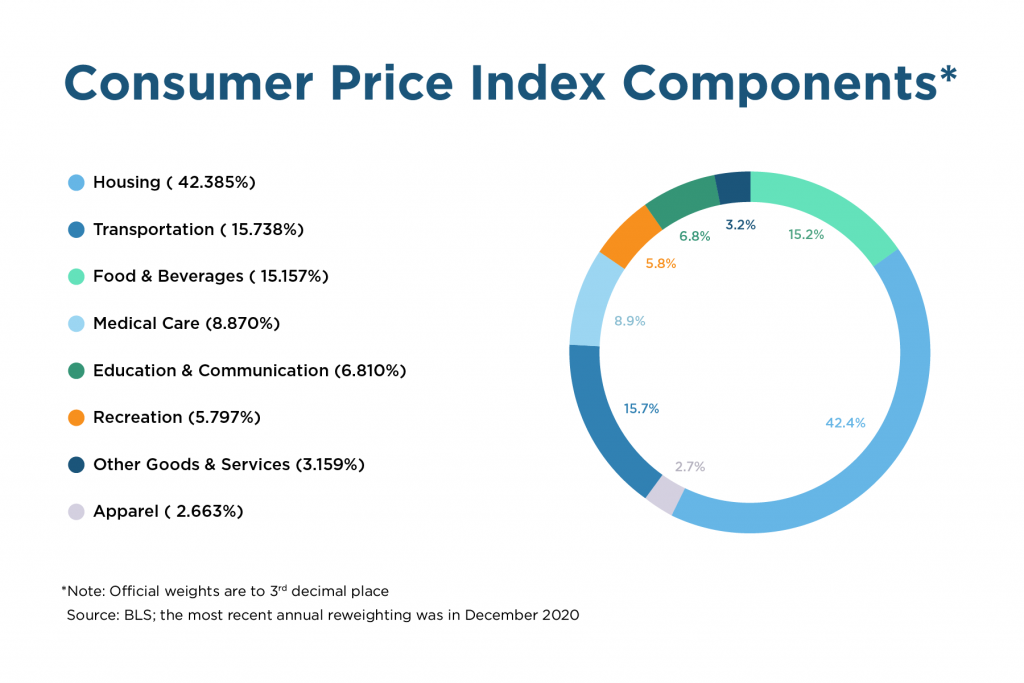

The Bureau of Labor Statistics (BLS) tracks all the changes in the U.S. economy. To measure inflation regularly, the BLS created a representative group of things we spend money on, which they call a "basket." Think of it as the monthly expenses for an average U.S. household. The basket includes various categories, their relative "weights," and how much influence they have in the overall basket of goods and services.

The BLS then calculates the price changes in each of the categories every month and reports this information in the Consumer Price Index (CPI). The most widely reported version is headline CPI, which includes all categories. You will also see core CPI, which is headline CPI minus food and energy prices. The reason for this distinction is that food and energy prices tend to be very volatile, which can greatly affect the CPI in the short term.

A quick example

Let's say a trip to the grocery store in June of last year cost you $100. And this June - one year later - that same "basket" cost $103. This would be reported as a 3% year-over-year price change or 3% inflation.

It's important to know that inflation only measures the cost of things we buy day-to-day and doesn't include the price of assets or investments like real estate or stocks and bonds. Inflation is also a backward-looking number. It tells us very little about the future and nothing about how long a given level of inflation will last.

What this means for your financial roadmap

Headlines about rising inflation can get us all thinking about what moves we should be making with our money. Given that the United States hasn't seen a period of consistently high inflation in 30+ years, it's not something we are conditioned to think about. But every once in a while, inflation rears its head to remind us it's still there.

The good news is that there is one thing more powerful than inflation, economic growth, or the Fed's policies. These are all things we cannot control. So what is it? The decisions we make with our money every day. It's the things we can control - our spending habits, how much we save, how we invest, how much risk we take on, and how we plan for today and our futures - that will have the greatest impact on our lives. Yes, inflation is a concept we should all be familiar with, but it's just one facet of a much bigger picture when it comes to life and money.

The Facet Difference

At Facet, we believe that understanding economic concepts like inflation shouldn't require a degree in finance. We're here to translate the headlines into actionable steps for your life. While traditional firms might use inflation fears to sell you expensive products, we take a different approach. Our flat-fee membership model means our CFP® professionals focus entirely on your specific roadmap. We help you build a strategy that accounts for rising costs so you can focus on living well today, knowing your future purchasing power is part of the plan.