The recent breakout of major conflict in Iran has had a significant impact on world politics and the flow of global trade. Beyond the tragic human cost, these events have left investors grappling with how a potential regime change or a wider regional war could impact their portfolios. Here is how Facet approaches geopolitics in our investment analysis.

Respect the unpredictability

Military conflicts are notoriously difficult to predict. In this case, President Donald Trump has said himself that this conflict could be over in a matter of days or stretch out for weeks. Reports are that Central Command is preparing for the war to last until September. If the President’s advisors, with access to secret military intelligence, are uncertain about the outcome, those of us in the finance world need to remain humble about our ability to predict how these situations will play out in the markets.

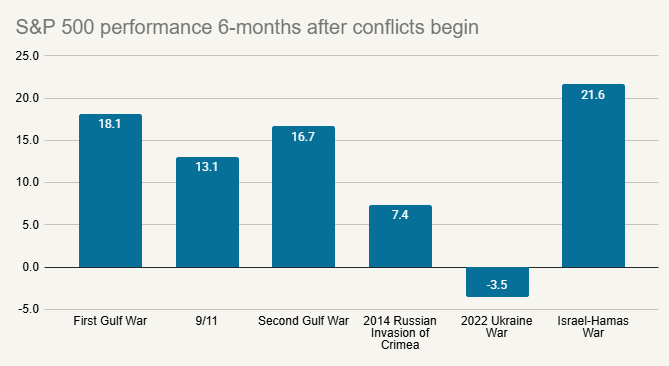

One simple way to see this unpredictability is to look at stock market performance surrounding major conflicts in the past. Historically, while the initial shock of a conflict can cause a dip, the S&P 500 has often trended upward in the six months following the start of hostilities.

Source: S&P Dow Jones Indices

This isn’t to say war is good for stocks. Rather other factors tend to matter more. It is important to put the impact of the conflict into context.

Facet approaches geopolitics by starting with a narrative exercise. We construct a "downside" story where something about the conflict impacts global growth negatively. Then we construct the opposite narrative, where the impact is contained or markets adjust quickly. This exercise helps us avoid putting too much weight on any one emotional outcome and reinforces just how much uncertainty exists.

Think in terms of macroeconomic impacts

When we analyze these narratives, we focus on the economic impacts. As we have often said, the primary driver of long-term stock prices is company earnings.

In other words, we have to think about how the war might impact everyday economic decisions. Will people buy fewer F-150’s from Ford? Will they be less likely to buy a Netflix subscription? Will businesses decide to not hire needed new staff? Generally speaking, most people and companies are probably going to make the decisions they would have made before this conflict began.

In the very short term, a few days or a week, the market may decline based on simple fear. But usually, within a month or two, that fear fades and the analytical machine of the market takes over. Actual company results become the driver again.

There may be impacts on individual companies or sectors. Does a conflict in Iran impact global defense spending? Likely. Does it fundamentally change the long-term demand for enterprise software or consumer staples? Probably not. We treat geopolitical narratives like any other macroeconomic scenario: we assess the size of the effect and compare it to what is already "priced in" by the market consensus.

Salience bias

Geopolitics carries heavy weight in an investor's mind due to salience bias—the tendency to overrate the importance of rare and notable events. The outbreak of a war feels like a monumental shift, so it feels like it must dictate market returns.

This can lead one to leap to the conclusion that if the Iranian conflict goes poorly it will be bad for stocks. We know this isn’t necessarily true. The post-9/11 conflicts in Afghanistan and Iraq did not turn out to be the quick and easy victories many assumed. This has had political reverberations to this day. Yet there was no material effect on financial markets.

While war is a major event in a human and political sense, it is not always a permanent driver for investment markets. By focusing on real economic effects rather than headlines, we avoid falling victim to this bias. Maintaining a strict, objective process is crucial to long-term investment success.

What about oil prices?

A conflict involving Iran immediately raises concerns about the Middle East, which accounts for roughly 30% of world oil production. With the current disruptions in the Strait of Hormuz, a corridor for 20% of the world’s seaborne oil, energy prices are a primary focus of our scenario analysis.

However, it is important to put this into context. Brent crude recently spiked toward $84 per barrel following the initial strikes, and there is a risk that oil prices keep climbing. Oil might be the single most important price for macroeconomics (if we don’t count interest rates), but even so, the relationship between oil and the broader economy is complex.

- Supply isn't the only factor. Oil prices came into this period relatively low, despite constrained supply from Russia, Venezuela and Iran, due to relatively weak demand for oil. This partly stems from the on-going construction bust in China.

- Energy is only one cost that businesses and households face. Oil prices probably only influence around 5% of producer costs and about 3% of household spending.

- The U.S. is a major oil producer. Higher prices can actually encourage domestic investment in the energy sector, offsetting some of the negative impacts on consumers.

Oil prices, inflation and the Fed

In general, the Federal Reserve focuses on so-called “core” inflation. That is, inflation excluding food and energy. So generally speaking, the Fed ignores short-term spikes in oil prices.

However right now inflation is already well above the Fed’s 2% target, which has some Fed officials feeling less willing to keep cutting rates. The war adds uncertainty to the outlook, perhaps making Fed officials even less likely to support rate cuts.

This might actually be the factor that ultimately matters the most for stock market investors. Before the attack on Iran, traders had expected either 2 or 3 rate cuts in 2026. That has receded to more like 1 or 2. The stock market can perform quite well even if the Fed doesn’t cut rates, presuming the economy is strong otherwise. But if the economy softens, the market is going to look to Fed rate cuts to help give the economy a boost. It is possible that spiking oil prices get in the way of how the Fed would normally react.

We think this emphasizes our point above about focusing on the economy rather than the conflict. The strength of the economy and company profit growth is the primary factor to watch. The Fed is a secondary factor, and perhaps oil prices could have some influence on that secondary factor.

The danger of getting out of the market

Geopolitical tension often creates a temptation to reduce your stock holdings until things settle down. However, this is a form of market timing that is historically problematic.

Consider all of the other geopolitical conflicts of the last 30 years. Our chart above shows that had an investor sold their portfolio they would have missed the significant rallies that followed. Once you sell, it can be extremely hard to get back in, which can create a major long-term impairment in your portfolio.

There is always a reason why stocks might go down. If you wait for the world to be free of conflict before investing, you will likely never get your money working for you.

At Facet, we don't ignore geopolitics, but we do insist on putting it into proportion. Our process is designed to look past the immediate noise and build portfolios based on objective, long-term analysis.