The Federal Reserve held their first meeting with Kevin Warsh as Chair on June 17. Warsh comes into the job with many challenges. Warsh himself has said he wants a “regime change” at the Fed, and said he plans on being “reform-oriented, abandoning old models.” Now that he is Fed Chair, we’re going to find out more about what changes he actually intends on pursuing, and how those might impact your portfolio. Here are our thoughts on what Warsh said at his first press conference, and what might come next.

Will the Fed hike rates in 2026?

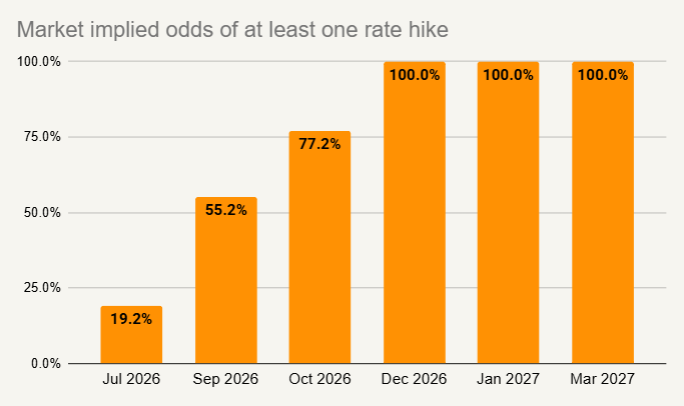

While future policy is never guaranteed, current market data suggests the Fed could hike rates at least once by late 2026 or early 2027.

The chart below shows the market-implied odds of at least one rate hike of 0.25%, according to the futures market. As of the evening of June 17 (just after the Fed meeting) the market is pricing more than a 70% chance of a hike by the October meeting, and more than 100% chance by the December meeting.

Source: CME Group

These expectations were reinforced by the so-called “dot plot” released with this meeting. This is where each member of the Fed’s Committee puts where they would personally prefer rates be set in the future assuming their own economic forecast comes to fruition. Half of the Committee penciled in a hike by the end of 2026, with six members suggesting multiple rate hikes this year.

In addition, the minutes from the Fed’s April 2026 meeting indicated that a “majority” of Committee members believed rate hikes would be "appropriate" if inflation kept running above 2%.

During his first press conference, Warsh did not strongly indicate whether he anticipates rate hikes in future meetings. He went out of his way to say that he didn’t intend on giving “forward guidance." He did say that when his colleagues filled out the “dot plot” survey, they did so with “pencil.” Meaning, a lot will happen in the economy over the next several months. Odds are good that the case for or against rate hikes will become a lot more clear depending on how the economy behaves. Warsh doesn’t want to overpromise now, when the outlook has so much uncertainty.

Why is the Fed considering hiking rates?

The Fed is leaning toward rate hikes due to a combination of improving economic growth and rising inflation.

At the start of 2026, investors were anticipating rate cuts over the course of the year. A lot has changed since then:

- Job growth has improved: Net job growth was negative over the second half of 2025. So far in 2026, the U.S. has added an average of 114,000 jobs per month. This has the Fed less worried about the state of the labor market.

- Consumer spending has been strong: So far in 2026, consumer spending growth has advanced at a 7.8% annualized pace. If that keeps up through the whole year, it would be the strongest growth for consumption since 2021.

- Inflation has increased: Core PCE inflation has been above the Fed’s target consistently since 2021, however in 2025 there was good reason to think inflation was subsiding. Instead, inflation has accelerated in 2026, with the most recent Core PCE inflation figure coming in at 3.3%, highest since 2023.

With oil prices down, will inflation subside?

Even if oil prices keep falling, core inflation could stay high.

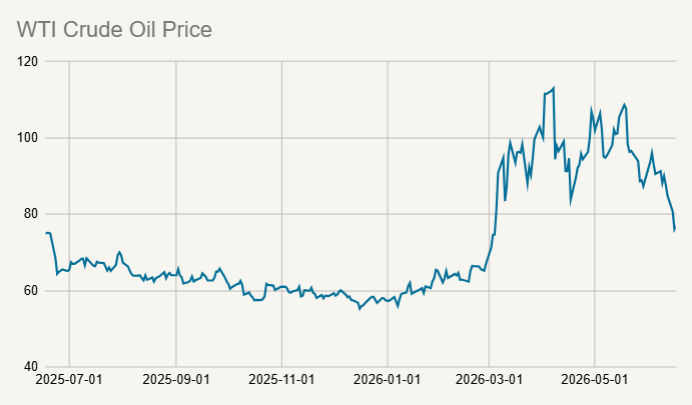

In the days leading up to the Fed’s June meeting, the U.S. and Iran agreed on a “memorandum of understanding”, which should allow the Strait of Hormuz to reopen. This has led to a significant drop in oil prices. After peaking at $113 at the height of hostilities, crude oil has fallen to just below $80 as we are writing this article.

Source: CME Group

Unfortunately, falling oil alone may not solve the Fed’s inflation problem. “Core” inflation - which strips out food and energy prices - has risen at a 3.3% rate over the last year. That’s far above the Fed’s 2% target. So even excluding the impact of things like spiking gas prices, inflation overall is still much too high.

One caveat is that core inflation only excludes the direct impact of oil on inflation. There are probably meaningful indirect impacts. For example, if higher oil increases the cost of shipping goods, that could raise the price of all kinds of items. Such an effect would influence core inflation, even though really it was an energy-related impact.

That being said, any easing of energy-related pressure probably won’t be enough to forestall Fed rate hikes. Oil prices are still well above where they were pre-war. In addition, history suggests that once companies raise prices, they tend not to cut them later. That could mean that price hikes on things like clothing or building materials remain sticky even after oil prices fall.

Will Kevin Warsh cut or hike interest rates?

During 2025, Kevin Warsh spoke a lot about wanting to cut rates, however economic conditions may have changed his mind.

As President Donald Trump was considering who to nominate as Fed Chair, he made no secret of the fact that he wanted someone who would cut rates. Perhaps knowing he was auditioning for the job, Kevin Warsh has consistently stated a desire to get rates lower over the last couple years.

This may belie Warsh’s real economic views. As we discussed in a prior article, Warsh has historically acted as a “hawk”, i.e., someone who tends to prioritize fighting inflation over promoting employment. This attitude would usually lead to more rate hikes, not more rate cuts.

Since taking the job at the Fed, Warsh has hired Paul Winfree as one of his advisors. Winfree has advocated for eliminating the Fed’s employment mandate altogether to allow complete focus on inflation. Exactly what influence these advisors will have isn’t clear, but it does suggest Warsh is surrounding himself with people who might favor hiking rates given how high inflation is currently.

When Warsh was formally sworn in as Fed Chair in May, President Trump said the new Chair should “do whatever he wants.” It appears Warsh is doing just that.

How might Kevin Warsh change the Fed?

There are a number of reforms Warsh may pursue at the Fed, and these could have major changes for investors and the economy.

- Press conferences: Warsh has suggested he may not hold a press conference after every Fed meeting. He said that Fed officials should “stop talking so much” and that “if one has a press conference, one wants to deliver some important news.”

- Forward guidance: The Fed has historically tried to telegraph to markets their future intentions, so that generally investors know the Fed’s next move weeks or even months before it happens. Warsh has said that this results in the Fed hanging on to forecasts longer than they should. In other words, he argues by trying to avoid surprises, the Fed becomes boxed in by prior promises. We got at least one hint about how Warsh will handle communications: the Fed’s press release was dramatically shorter than these releases have been in recent years.

- Dot plot: Earlier we mentioned the “dot plot” where each member of the Fed committee gives their own views on rates. Over the years this exercise has had lots of critics, Warsh being just one of them. Scrapping the dot plot might be the easiest change Warsh could make to reduce the amount of forward guidance the Fed gives.

- Balance sheet: After the 2008 Financial Crisis, the Fed began to mandate bank hold much larger reserves at the Fed. This has resulted in the Fed’s assets ballooning. Critics, including Warsh, say this has resulted in distortions in the bond market and potentially the broader economy. It will take quite some time before the Fed can practically make meaningful changes to the balance sheet, however. Since the balance sheet and banking regulations are tied together, Warsh himself has said the Fed will move slowly and carefully study any change to the balance sheet.

- Trimmed mean inflation: The Fed uses “core” inflation because they want to strip out very volatile food and energy prices. This is because the volatility of those items can distort the underlying trend in general inflation. Warsh has suggested taking this a step further and using “trimmed mean inflation.” This is an inflation measure where you always take out the most volatile items each month, regardless of what category those prices come from.

During the press conference, Warsh said he was appointing several task forces ranging from Fed communications, data gathering, and the Fed’s balance sheet. It seems these task forces are aimed at fleshing out how these reforms could be carried out in practice. Warsh said he hopes these task forces will complete their work by the end of the year.

How can you protect your portfolio from rate hikes?

Fed rate hikes aren’t necessarily a problem for investment markets, but there are some considerations for your money.

Remember that the #1 driver of stock market performance is company profit growth. Therefore stocks would rather see a strong economy, even if that means Fed rate hikes. This is why stocks have had such a good 2026, despite the increasing threat of rate hikes. Any negative impact of higher interest rates has been more than offset by stronger profit growth.

That being said, there are some corners of the market that tend to struggle with rising rates.

- Speculative tech stocks: Companies that are growing quickly but have modest (or even negative) profitability today could be most at risk. That’s because these stocks have a lot of their value in far-off projected cash flows. We saw this play out in 2022, where smaller tech stocks (a good proxy for more speculative stocks) fell 36%, far worse than the -28% for larger tech companies, and -18% for the broad S&P 500.

- Bonds: While bond prices tend to fall when rates are rising, there is a silver lining for bonds. The reason why bonds performed so poorly in 2022 was because the Fed had let inflation get out of control in 2021. They were then forced to hike extremely aggressively to get prices back under some kind of control. If the Fed acts more proactively this time, and inflation stays reasonably contained, that could prevent the need for a larger number of hikes. This in turn could keep bonds performing reasonably well.