A vast body of data suggests that picking winners in the stock market is extremely hard. Academic research in the 1960’s and 1970’s first provided some evidence that most active portfolio managers fail to outperform the broad market. This led to the popularization of index funds during the 1980’s and 1990’s, which continues today. However, the allure of “beating the market” or finding big winners in single stocks can be hard to resist. A large percentage of portfolios that come to Facet, either from other advisors or individuals investing on their own, own significant amounts of individual stocks.

At Facet, we don’t believe picking stocks adds value to portfolio construction. We believe owning the whole market, either through exchange traded funds or direct indexing, with some tweaks based on the balance of risk and reward, improves your chances of long-term investment success. In this article, we’ll discuss a variety of reasons for why picking winning stocks is so difficult, and why you should probably avoid trying.

Can professional investors pick winning stocks?

There is scant evidence that professional investors can beat the market. In fact, the long-term record of professional stock pickers is surprisingly poor. According to SPIVA, only 14% of U.S. actively managed funds have outperformed the S&P 500 over the last 10 years

This is remarkable when you consider the resources that fund companies have to help analyze which stocks to buy. A typical fund has all of the following:

- One or more portfolio managers: usually with 20+ years experience as investment professionals.

- A dozen or more stock analysts: generally tasked with covering a sector or industry. They do nothing but analyze companies in that sector all day every day.

- Expensive data and technology: This includes everything from price history to company reports to non-traditional data like credit card spending or satellite location data.

Even with all of those advantages, very few fund managers have actually outperformed simple index funds.

Do top performing investment funds stay at the top?

Unfortunately, outperformance by money managers usually doesn’t persist from one period to the next.

If we were to assume there was some kind of skill to stock picking, you would think the manager who outperformed last year would be a good bet to outperform next year. This is how most “skills” we observe work. Someone who is a good lawyer in one trial is probably going to still be a good lawyer the next trial. A tennis champion from one tournament has a pretty good shot to win the next tournament.

But with stock picking, this just doesn’t seem to be the case. Researchers at SPIVA analyze the persistence of fund outperformance. They took the top 25% U.S. fund performers from 2021 and tracked performance through the end of 2025. Over this specific period, none of the funds that started out as top performers remained in the top quartile for that period

You have probably heard the phrase “past performance is not indicative of future results.” This really applies to any type of investment, but when it comes to picking individual stocks, this takes on a particular meaning. Stock pickers often market past outperformance as a reason to buy their fund. However, remember that when you pick a manager, you don’t get the manager’s past results. You only get the future returns. The data suggests that past outperformance doesn’t indicate much of anything about future potential outperformance.

What percentage of individual stocks actually beat the market?

Most stocks actually underperform the broad stock market, with a few winners carrying the market averages.

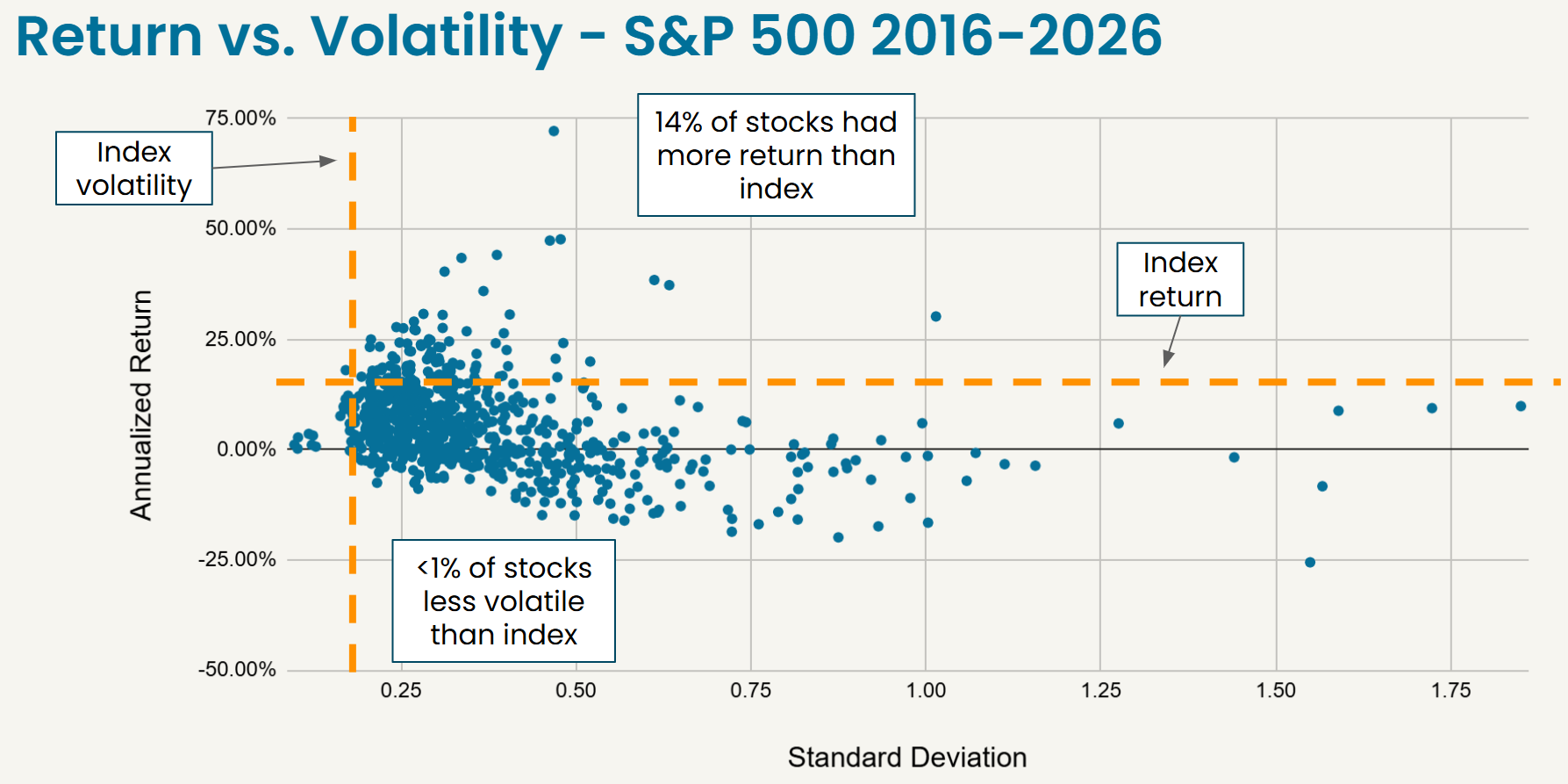

This is a key reason why stock picking is so difficult. For the 10-years ending April 2026, the S&P 500 was up 15.2% per year. Of all the stocks that were in the S&P over that period, only 14% of them produced better returns than 15.2%. The chart below shows the return and volatility of all stocks that were part of the S&P index over that 10-year period.

Source: Dow Jones S&P Indices

This might be a bit counterintuitive. One might assume that if the average stock was up 15%, then about half would be better than that and half would be worse. However in reality, stock returns aren’t evenly distributed.

Some of this is due to the math of compounding:

- A stock can only go down by -100%, but it can go up by a much greater degree.

- The best performing stock over this period was Nvidia, which was up a total of 22,842%!

- In any given period, there are going to be a relatively small number of huge market winners.

- These big winners carry the index’s overall return.

This means that missing the big winners is a much bigger problem than owning too many of the losers. You can get away with owning a large number of underperforming stocks as long as you also own the big outperformers. This is one of the key benefits of owning a highly diversified portfolio - the more of the market you own, the more likely you are to own the winners!

How can I find the next Nvidia?

You hear a lot of claims about which stock is going to be the next Amazon or Tesla or Nvidia, but there is no reliable way to identify which stocks will be tomorrow’s big winners.

In fairness, there is a certain profile of a stock that could be a big winner. It tends to be companies with big potential but high uncertainty. Unfortunately, those kinds of companies also tend to be highly volatile. If a company’s future is uncertain, the value of the company today is also uncertain, which tends to lead to big price swings.

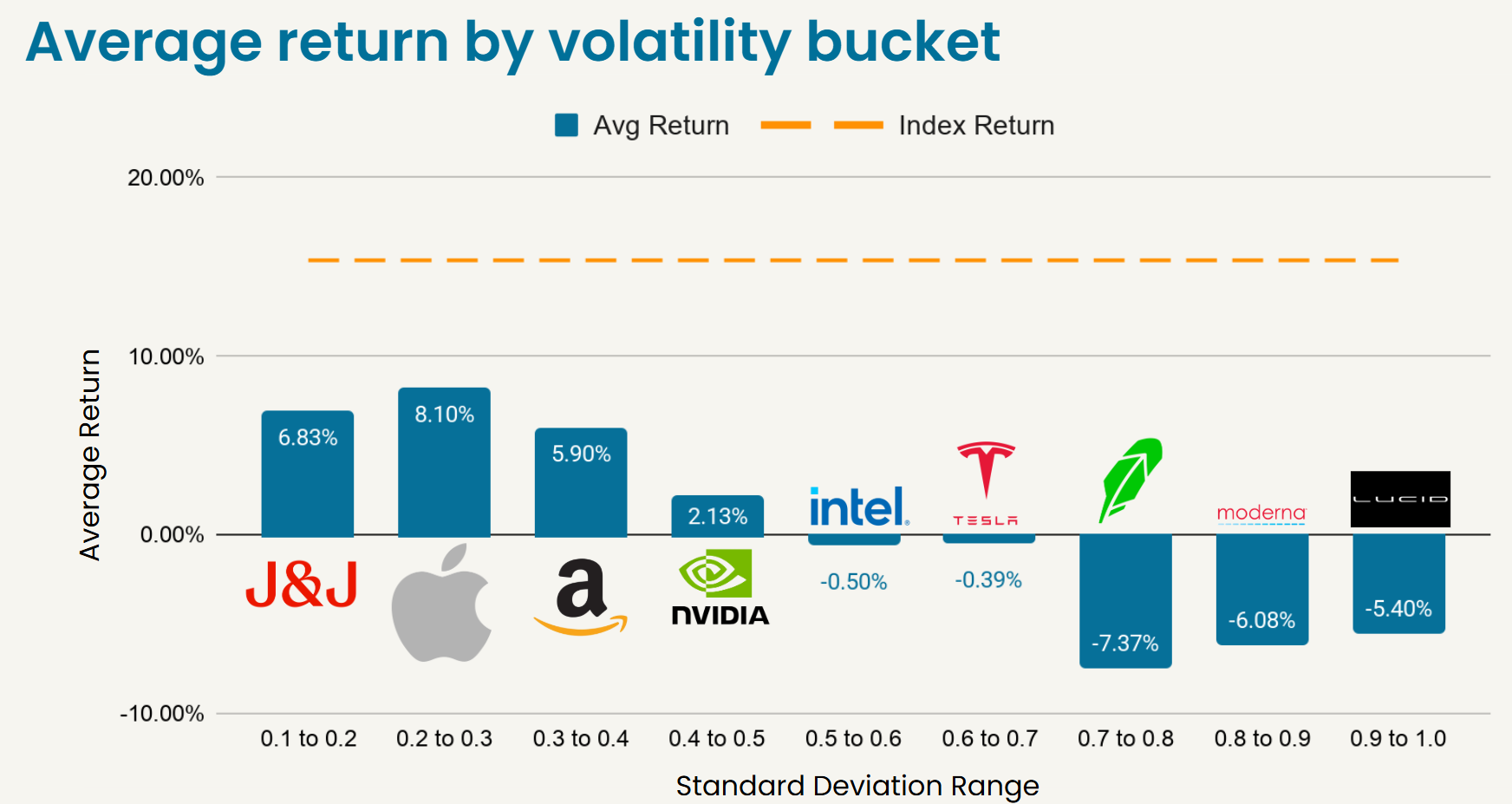

In the chart below, we grouped all companies that were in the S&P 500 over the last decade into volatility buckets. We added the logo of the biggest company in each bucket. Effectively, this is who the “winner” was within that bucket. The blue bars are the average stock return within that volatility range and the orange line is the average return for the whole S&P 500.

Source: Dow Jones S&P Indices

In a sense this chart tells you what would have happened if you tried to pick a stock that was “like Nvidia” or “like Tesla.” The average company with the same volatility as Tesla lost money over the last decade.

One way to think about this is for every Tesla that produces a huge upside return, there are dozens more companies that have similar upside potential but don’t realize that potential. This means the odds are against you - there are 2-3 big winners and a whole lot of losers in each of these buckets.

Is it risky to only invest in the biggest tech companies?

You probably should have a healthy allocation to today’s big tech companies, but it isn’t all you should own.

It is very difficult for any company to sustain success decade after decade. Every company deals with shifting customer preferences, new competition, cost pressures, changing regulations, etc. Any of these factors and dozens of others can cause a once dominant company into an also-ran.

Nowhere is this more true than in tech, where companies also deal with a rapid cycle of new innovations and obsolescence. Here is a list of the 10 largest tech stocks in the S&P 500 from 25 years ago:

- Microsoft

- Intel

- IBM

- Cisco Systems

- Oracle

- EMC

- Dell

- Texas Instruments

- Sun Microsystems

- HP

Of these, only one (Microsoft) is still in the top 10 tech stocks within the S&P 500 today. Even if we only rewound 10 years, just 5 of the top 10 tech stocks from 2016 are still in the top 10. Today’s most valuable company, Nvidia, was the 237th most valuable company in the S&P 500 in 2016. At that time Nvidia primarily made products for video gamers, not the cutting edge AI tech company we think of it being today.

If you own a concentrated portfolio in today’s biggest tech stocks, you effectively own a portfolio of yesterday’s winners. It is unlikely that all of them will be tomorrow’s winners.

Is picking individual stocks worth it?

Investing should be about maximizing the chance you reach your financial goals. That isn’t exactly the same thing as trying to maximize the return on your investments.

A lot of times when individual investors get wrapped up in single stock picking, it is because they are chasing higher returns. The problem is that doing this comes with a lot of downside risk, either outright loss or the risk of poor performance.

A highly diversified portfolio helps to narrow the band of potential returns, which in turn could help boost the chances that your portfolio earns an adequate return to meet your goals. For example, if retiring on time is your goal, we would argue that trying to get there by picking a handful of single stocks lowers your odds. This is the benefit of index funds vs. stock picking.

It is fun to try to pick that next big stock winner, but we believe stock picking is closer to gambling than it is to investing. The data backs that up. Most stocks perform poorly. Maybe you will get lucky, but the data suggests you probably won’t.

Disclosure: This is intended to be a general analysis and not a recommendation or advice. Any investment advice would be specific to your personal situation. All investing carries risk including the loss of principle. Past performance is not indicative of future performance and there is no guarantee of outcome. For most long-term investors, broad diversification provides a mathematically sound baseline to capture broad market returns compared to predicting individual stock winners. However, diversification does not ensure a profit or protect against market loss in a declining environment. Index performance results cited reflect the reinvestment of dividends but are presented gross of any advisory fees, management fees, trading commissions, or administrative expenses.