A major question for those thinking about retirement is how much can I afford to draw from my account? This is a complex question, involving a lot of factors. There are some helpful basic guidelines or rules-of-thumb that could be a good place to start. However, these are usually too simplistic for most real-life situations. Here are some things to think about as you consider your own retirement plan.

What is the 4% rule for retirement withdrawals?

The 4% rule is a very simple, generic rule for determining how much you can afford to withdraw in retirement.

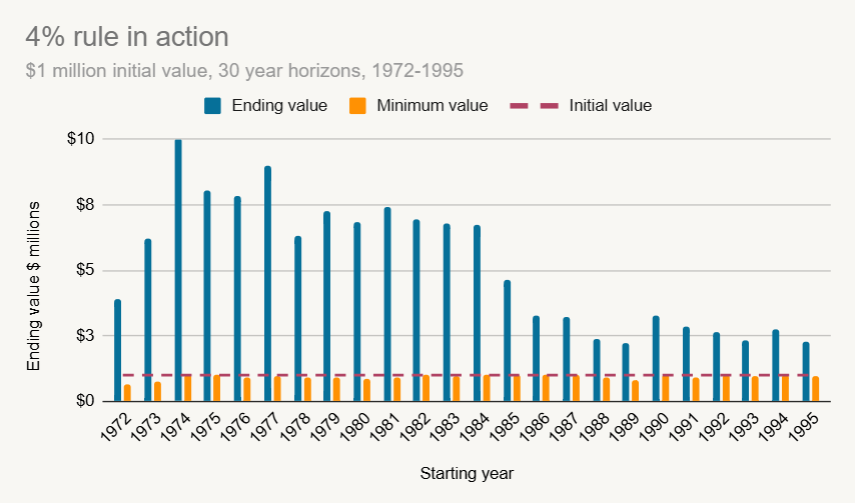

The rule was first articulated by William Bengen in a 1994 paper. The idea is that if you set your annual draw amount at 4% of your portfolio’s initial value, historically, there has been a strong probability that the funds will last over a 30-year retirement period. Bengen based this figure on historic observation, which we’ve replicated below. We created hypothetical portfolios from 60% equity, 40% bond portfolio, using the MSCI World and the Bloomberg Government/Credit Bond indices. We then tested 30 year horizons for each year starting in 1972. The portfolios start with $1 million in assets, and draw $10,000 per quarter (i.e., 4% of the portfolio’s initial value per year).

In the chart, you can see that using a 4% draw rate, this portfolio didn’t run out of money any of our simulated 30-year periods. In these specific scenarios, the portfolio consistently ended with more than the initial $1 million.

The 4% rule is a good place to start when you are thinking about withdrawals from your portfolio in retirement. However, there are several reasons why a simple 4% draw rate might not fit your specific situation:

- Inflation and taxes: your draw rate doesn’t just have to cover today’s living expenses, but also taxes and future inflation.

- Retirement age: if you retire younger, you may need a more conservative draw rate. If you retire older, you can be more aggressive.

- Timing of other income: when does Social Security start for you? What about pension income, annuities, etc.? Maybe you are expecting an inheritance or plan to sell a property. You may choose a larger draw in the early years of retirement while waiting for these other income sources to kick in.

- Legacy goals: Some people want to maximize retirement spending. Others want to preserve their portfolios to give to their heirs or to charity. These choices make a big difference in how you might want to draw from your portfolio now.

- Spending flexibility: You may be able to draw more from your portfolio if you can afford to cut back spending during down markets.

These factors and others are what makes your retirement plan very specific to you. While the 4% rule is a good starting point, it probably won’t fit your situation exactly right. Here are a few details on some of these key issues in determining how much you can actually afford to draw from your portfolio.

How can you protect yourself against inflation in retirement?

Inflation can be a major problem for retirees, and protecting yourself requires careful planning.

In the chart above, we assumed a $40,000 level draw amount each year for 30 years. However, that assumption doesn’t take into account inflation. For example, the same basket of goods that cost $40,000 in 1972 would have cost $171,106 in 2002, based on Consumer Price Index (CPI) data.

In other words, if 4% covers your living expenses today, your actual plan needs to assume a growing draw rate to cover inflation.

Considerations for portfolio inflation protection:

- Be careful with investment strategies that purport to protect against inflation. Many times these strategies either harm the growth rate of your portfolio and/or haven’t historically always performed well during inflationary periods.

- Large bond allocations could create inflation risk. Many target date funds have 50% or more in bonds by the time you get to the “target” date. The problem is that bonds have historically underperformed during high inflation periods. In addition, they tend to have less growth potential than stocks.

- Focus on growth potential. In our view, the best approach to inflation protection is to build a portfolio with enough growth potential to allow for a growing draw rate. Instead of focusing on “hedges,” focus on a retirement plan that could be resilient to a bout of higher inflation.

How do taxes impact your retirement portfolio withdrawals?

Your tax bill in retirement can vary substantially depending on how you structure your portfolio withdrawals. Careful planning can allow you to keep more of what you have earned.

How your withdrawals will be taxed depends on what type of account you are using:

- Brokerage or other taxable account: You will pay the capital gains rate only on your gains.

- Traditional IRA, 401(k) or other employer plan: You will pay the ordinary income tax rate on the entire withdrawal amount.

- Roth IRA: You pay no taxes on withdrawals.

- Health Savings Account (HSA): You pay no tax on withdrawals as long as the money is used for qualifying medical expenses.

To illustrate how much this can matter, consider a retiree in the 24% Federal tax bracket drawing $100,000 for living expenses. To fund this withdrawal, they sell some investments that have appreciated by 50% over time. Below is how much this investor would owe in taxes in different account types:

- Taxable account: $7,500 estimated Federal tax (Assumes 15% capital gains tax rate on $50,000.

- Traditional IRA: $24,000 estimated tax (Assumes 24% ordinary income rate on the full $100,000).

- Roth IRA: $0 tax. (No taxes on either the sale of the funds or the withdrawal).

A smart retirement plan includes a strategy for what accounts you will draw from when. The right planning can help you keep more of your portfolio’s value for your own retirement, as opposed to paying it to the IRS.

What is sequence of return risk in retirement?

Sequence of return risk is the risk that the market will suffer a large decline in the early years of retirement.

Historically, the stock market has averaged something like 7-10% per year depending on the exact index and time frame you use. You might think this suggests you could draw 7% of your portfolio each year without ever risking draining your portfolio. Unfortunately, that would be extremely risky. The problem is timing.

Once you start drawing on your portfolio, you are no longer truly a “long-term” investor. At least some portion of your money becomes short-term in nature. Because of this, market volatility takes on new importance for retirees. We know the market is going to have good years and bad, but we don’t know when good or bad years are coming. This timing really matters.

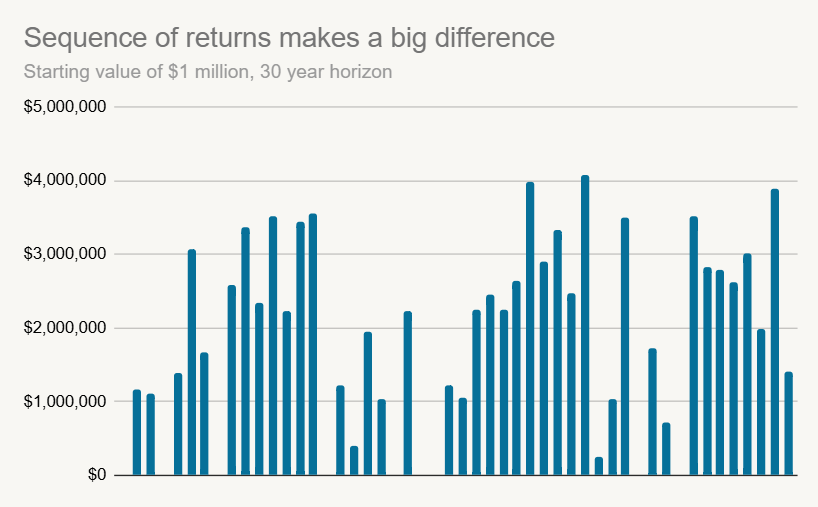

To illustrate this, we ran 50 random simulations of 30 year horizons. In each simulation, there were exactly 6 negative markets where a hypothetical portfolio fell by -20%. There were 24 positive markets where our portfolio makes +15%. As a result, all 50 simulations had exactly the same average return of 7% per year. We assumed a $1 million starting value, drawing $40,000 per year. We increased the draw by 3% per year to account for inflation.

The chart below shows the ending value for each of our random 50 simulations.

Source: Facet calculations

The ending market value in this exercise was over $3 million in 24% of simulations, but in 18% of simulations, the hypothetical investor ran out of money completely. The only difference was either lucky or unlucky timing.

Sequence of return risk is a big part of effective retirement planning, involving many elements. However, selecting a sustainable draw rate is key. It is important to stay disciplined and not allow your draws to drift higher in good markets. That could impair your ability to withstand down markets.

How can I maximize my retirement portfolio withdrawals?

To help maximize your spending ability, building on-going flexibility into your financial plan is critical.

Some people want to maintain the value of their portfolio so they can pass their estate on to their children. Others will say they want to enjoy their money in their lifetimes. It is the old saying: “I want the last check I write to bounce.”

The more aggressively you are spending your retirement portfolio, the more sequence of return risk matters. Say you start out with $2 million, drawing $120,000 to fund your lifestyle. In a steady market, that draw rate is plenty sustainable. But what happens if there’s a 25% market decline right after you retire? Suddenly your portfolio is worth only $1.5 million. Unless the market rebounds in short order, the $120,000 draw will become unsustainable very quickly.

Here is where ongoing planning is really important. You may have to adjust your spending rate during down markets. Alternatively, you might have a plan to spend at a higher rate early in retirement, and then slow down later. You might even create a couple paths depending on how the market performs. These could involve spending adjustments or things like selling a property.

It is very unusual for someone’s retirement to go exactly to plan. This is why it can be helpful to regularly revisit the plan and make adjustments as necessary.

How do I determine the right retirement withdrawal rate for me?

Coming up with a sustainable retirement withdrawal rate for you requires developing a comprehensive, ongoing retirement plan.

There are several ways to approach determining your retirement draw rate. You might start by estimating your expenses, then aim to determine if your portfolio can cover those expenses. Conversely you could try to determine a safe draw rate given your assets, and try to make your expenses fit that figure. From there you can adjust variables like your asset allocation, timing of your retirement, considering things like part-time work, etc.

At Facet, we believe a key to retirement success is having confidence in your plan. It is a big psychological shift to go from earning a steady paycheck to feeling like you are at the mercy of fickle financial markets. A comprehensive plan to start, and then ongoing revisions to that plan as your life evolves, could help you have the confidence in your retirement plan.

Disclosure

All statements, data and graphs above are intended to be illustrative and are not advice or a recommendation. Any advice should be specific to your individual needs and circumstances. There are inherent risks with investing including the loss of principal and past performance is no guarantee of future results.