When we talk about investing at Facet, we always start with the same foundation: Your portfolio should be designed to achieve your specific life goals.

It sounds simple, but it requires a careful balance. We want to maximize the chance you reach those goals, which means seeking growth. However, we also need to protect your savings from other risks, including inflation or sudden market declines. Each of these risks is different for you depending on where you are in your own financial journey. The key risks for a young couple just starting out is very different from someone about to retire. Hence this requires a strategy that adapts not only as your life changes but also as the world around you changes.

This is why we believe a dynamic portfolio—one that adjusts as conditions change—is often superior to a static set of funds or a "set it and forget it" target date fund.

Why not just "buy everything"?

We have written before about the dangers of trying to "time the market" by guessing things like whether AI stocks are in a bubble. It is nearly impossible to predict the future with precision. However, there is a big difference between guessing the future and recognizing the present. We can look at the market right now and see when there might be an imbalance between opportunity and risk.

When the risk of a specific asset class outweighs the potential reward, a dynamic portfolio moves money away from that danger. Conversely, when there is more opportunity relative to risk in some market segment, we can add to that segment.

Small-cap stocks (companies with smaller market capitalizations) are a current example of someplace where we think the risks outweigh the reward.

- Historically, small companies have been a driver of growth, especially during economic rebounds.

- Right now, however, they are uniquely vulnerable. If the economy slows, small companies often lack the financial flexibility to adapt.

- In addition, if there is a "tech bust" perhaps driven by an AI bubble bursting, small caps are also at risk, because a significant portion of the small-cap universe consists of unprofitable technology companies.

Despite these risks, small-cap valuations are high, sitting well-above the 20-year average in terms of their Price-to-Earnings (P/E) ratio. We argue this implies the upside to small companies is relatively limited.

In our view, the risk currently outweighs the reward. A static portfolio has no way of adjusting to this new reality. A dynamic approach allows us to reduce this exposure.

How do market risks change over time?

One of the biggest flaws in building a "forever portfolio" is that we tend to build it based on assumptions colored by the recent past. But the economy is not static. A strategy that protects you in one decade could potentially diminish in the next.

Historically, several static strategies have struggled when economic conditions shifted:

- Value and small cap: In 1992, Eugene Fama and Kenneth French published a paper arguing that “value” stocks and smaller companies produced better long-term returns. They claimed this was for structural reasons that would persist into the future. Over the next decade, this approach would become popular among advisors. French himself became an advisor to a mutual fund company that followed this research. However over the last 20 years, small value stocks (such as the Russell 2000 Value Index) have produced less than half of the return of the S&P 500.

- “Equal-weighted” strategies: After the dot-com bust, “equal-weighted” portfolios became popular as a way to make sure no one stock or sector became too large. A large number of funds were launched in the late 2000’s to follow this strategy, with many advisors following suit. Since 2010, the Russell Equal-Weighted index has underperformed the standard-weighted S&P 500 (14.1% vs. 11.2% through April 28).

- Deflation hedges: After the 2008 financial crisis, loading portfolios with very long-term bonds became very popular. The idea was to build portfolio defense against deflation, which had seemed like the primary worry after 2008. However the next major crisis, the COVID pandemic, brought on an inflation spike. That caused long-term bond prices to plunge in 2022 at the same time that stocks also fell. The popular Vanguard Long-term Treasury ETF fell 29% that year.

In each case, the argument for these approaches was backed up by considerable historic evidence. However, if you adopted any of these approaches, how do you know when to make a change? Fama and French’s data went back to the 1960’s, so five years of underperformance didn’t change the overall conclusion. What about 10 years? What about 20? By the time you realize you are wrong, you may have suffered quite a lot of underperformance.

This is why we prefer an approach that is flexible, and focused on current conditions. When you use these long historic studies to make investment decisions, you are inherently assuming the future will be like the past. Yet we know the economy is radically different today than it was 20, 30 or 40 years ago. When Fama and French were doing their analysis, the internet didn’t even exist, much less something like AI.

Historic data can certainly be useful in investment analysis. However, we prefer to start with thinking about the future rather than the past.

Why not just hold the S&P 500?

Maybe you are holding a portfolio dominated by an S&P 500 fund. Such an approach has been extremely successful over the last decade, as large U.S. companies have outperformed almost all other corners of the global stock market.

However we don’t think this approach is maximizing the chance of reaching your goals. Just because large U.S. companies have been the winners in recent years doesn’t mean that will continue into the future. In 2025, non-U.S. companies outperformed substantially. The Morningstar Developed Markets ex. U.S. was up 31.6%, far ahead of the S&P at 17.9%. This has been due primarily to the dollar weakening. Could the dollar keep weakening into the future? Maybe, or maybe not. But if you want to maximize the chance of your portfolio achieving a certain baseline return, spreading out your holdings to include some non-U.S. dollar probably makes sense.

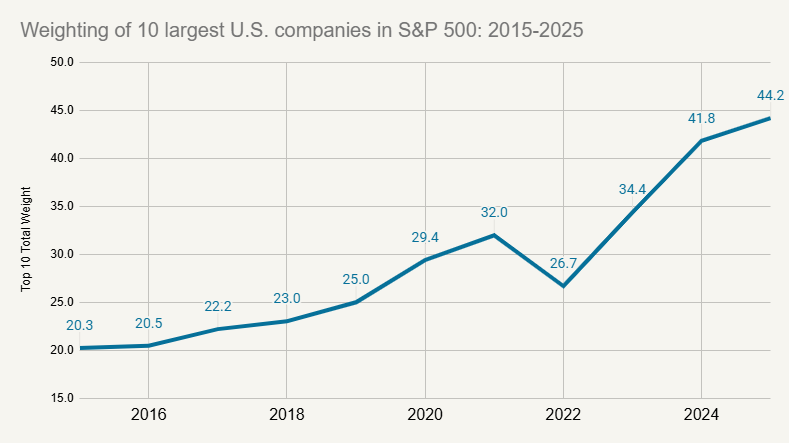

There’s another major risk of just holding the S&P 500: it has become extremely concentrated in just a handful of tech stocks.

The chart below shows the total weight of the ten largest companies within the S&P 500. A decade ago it was just 20%. Now it is 44%.

Source: Dow Jones S&P indices

Moreover, 8 out of the top 10 companies today are tech companies (or tech adjacent, such as Tesla). In other words, when you buy an S&P 500 ETF, more than 40% of your money is going into just 8 big tech companies.

This is another great illustration of how risks change over time. If you bought the S&P 500 ten years ago, you were getting a much more diversified portfolio than you are getting today. A static approach can’t adjust for these changing risks. A dynamic approach can.

What are the limitations of target-date funds?

For many investors, target date funds are the default choice in their 401(k). You pick the year you want to retire (e.g., 2030 or 2050), and the fund automatically becomes more conservative as you get closer to that date.

This suffers from a major flaw: It assumes your financial situation is identical to everyone else retiring that year.

But you are not the "average" person.

- Retirement Flexibility: What if you decide to work five years longer? Or retire five years early? The fund's "glide path" won't know that.

- Outside Assets: Do you have a pension? An expected inheritance? A spouse with a high income?

- Risk Capacity: If you have significant savings surplus to your needs, you might be able to afford more risk (and potential growth) than the fund allows. Conversely, if you have a medical issue requiring liquidity, the fund might be too aggressive.

If you have no other choice, a target date fund is "good enough." But when it comes to your life savings, you shouldn't aim for "good enough." You should aim for a strategy tailored to you.

Hitting the ball back over the net

In 1970, scientist and businessman Simon Ramo wrote a book titled Extraordinary Tennis for the Ordinary Player.

In it, he argued that there are two games of tennis. Professional tennis is a "Winner's Game," where the outcome is determined by who hits the most spectacular, unreturnable shots.

However, amateur tennis is a "Loser's Game." The outcome isn't determined by who hits the most winners, but by who makes the fewest mistakes. The player who simply focuses on keeping the ball in play—hitting it back over the net, time and time again—usually wins.

We believe this is the perfect analogy for investing.

Attempting to forecast the future or time the market is trying to play the “Winner’s Game.” Most of the time, investors who attempt this risk hitting the ball out of bounds and suffering losses.

Our dynamic approach is about playing the "Loser's Game" well. We aren't swinging for the fences. We are making small, calculated adjustments to keep your portfolio "in bounds"—avoiding overvalued sectors, managing risk, and keeping your investments aligned with your personal goals.

You don't need to be a hero to reach your financial goals. You just need a process that keeps the ball in play.